Most people still think of SpaceX as a rocket company.

That increasingly feels like looking at Amazon in 2006 and concluding it mainly sold books.

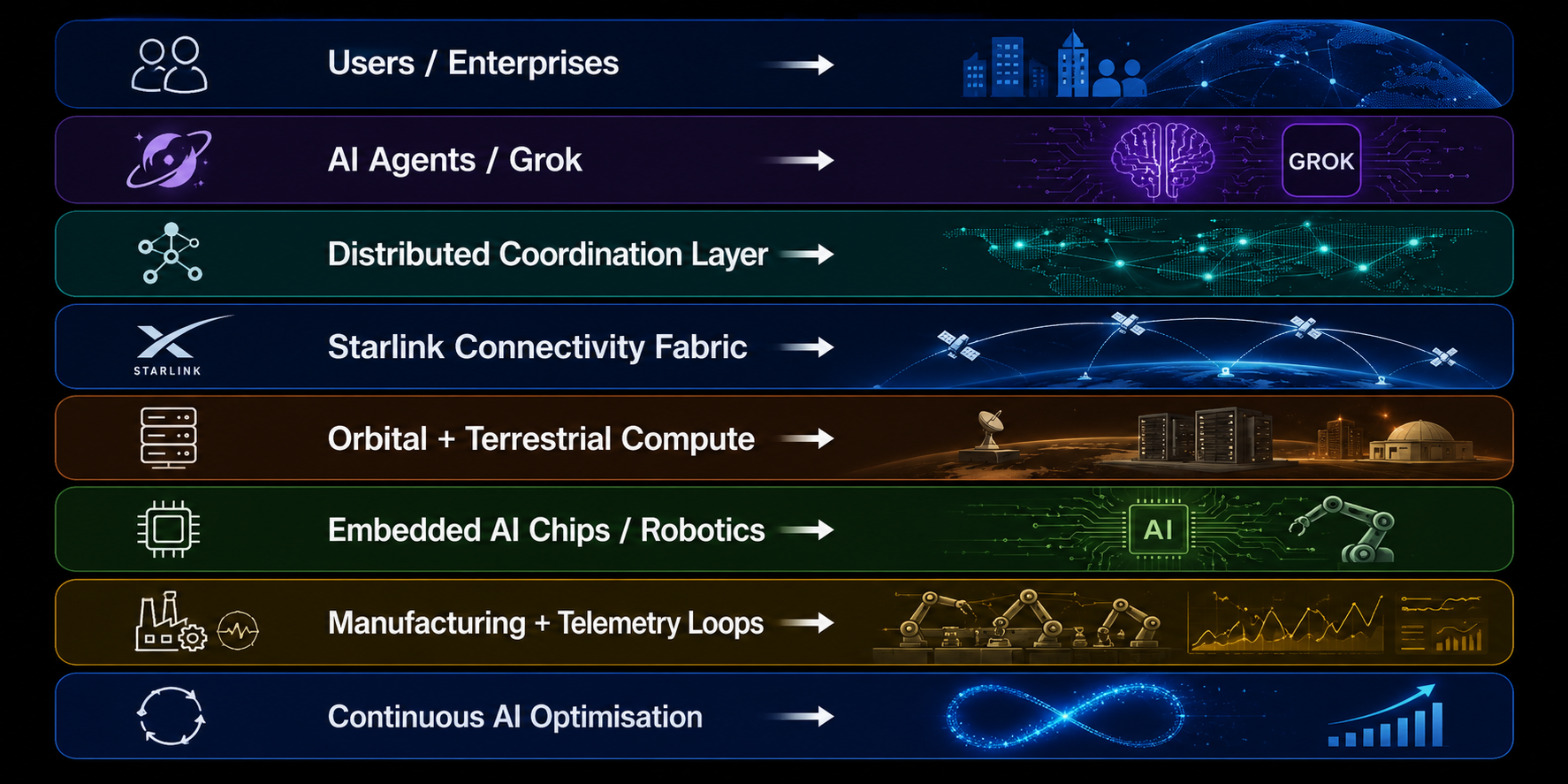

SpaceX is beginning to resemble something far larger: a vertically integrated infrastructure platform spanning connectivity, compute, orbital operations, AI models, robotics, manufacturing, and autonomous systems.

When a SpaceX IPO eventually materialises, investors may discover they are not simply buying exposure to launch economics or broadband.

They may be buying exposure to the early foundations of a globally distributed AI infrastructure stack.

And quietly, many of the layers are already appearing.

1. Connectivity: Starlink as the Coordination Fabric

Starlink is no longer simply a satellite broadband network.

It increasingly resembles a global low-latency coordination layer for distributed systems, autonomous platforms, robotics, vehicles, and persistent AI agents operating outside traditional terrestrial infrastructure.

As agentic systems evolve from isolated copilots into continuously operating digital workers, reliable low-latency communication becomes infrastructure rather than convenience.

That changes the strategic importance of global networking entirely.

2. Orbital Compute: The Infrastructure Economics of Persistent AI

Low Earth Orbit compute infrastructure is beginning to transition from experimentation into serious strategic discussion. As agentic AI expands, the economics of traditional hyperscale cloud infrastructure begin looking increasingly strained. Persistent AI agents generate continuous compute demand, real time coordination traffic, and enormous energy consumption. Centralised cloud regions were designed for applications making periodic requests. Agents behave more like distributed digital workers operating continuously. The economic model for AI infrastructure changes significantly when millions of autonomous systems begin generating persistent inference traffic instead of occasional user requests

3. Silicon: Edge Inference and Vertically Integrated Compute

At the same time, Tesla’s A15 AI chip strategy points towards intelligence moving directly into edge devices, vehicles, robotics, and autonomous systems. Embedded inference reduces dependency on remote cloud processing while enabling real time reasoning locally.

Terafab represents the next critical layer: silicon sovereignty.

The planned initiative involving Tesla, SpaceX, xAI, and Intel aims to vertically integrate large parts of the AI compute supply chain, including:

- chip design

- fabrication

- memory production

- advanced packaging

- testing

If successful, it would reduce dependency on fragmented semiconductor ecosystems while dramatically increasing long-term control over AI compute infrastructure.

[At time of writing neither Tesla nor TerraFab are part of the SpaceX IPO, but deeply linked]

How the emerging SpaceX AI stack starts fitting together

Starlink provides:

- Global low latency communications

- Mobile connectivity for distributed agents

- Persistent worldwide coverage

xAI and Grok provide:

- Frontier reasoning models

- Multi agent orchestration

- Tool use, memory, and autonomous workflows

- Persistent agent memory and coordination

- Autonomous operational reasoning loops

The fabrication plant provides:

- AI chip manufacturing capability

- Supply chain control for inference hardware

- Long term compute scalability

A15 class embedded chips provide:

- Local autonomy and reasoning

- Real time sensor fusion

- Edge based AI execution

Orbital compute provides:

- Distributed AI infrastructure in Low Earth Orbit

- Reduced terrestrial networking congestion

- Global synchronisation between agents

- Resilient distributed inference capability

- Reduced dependency on terrestrial hyperscale regions

Individually, each piece looks interesting.

Together, they begin resembling a new infrastructure model entirely.

Why This Matters for Enterprise AI

Most enterprise AI discussions still focus on models.

The larger shift may be infrastructure.

Persistent AI agents require:

- continuous inference

- low latency networking

- distributed coordination

- resilient compute

- embedded autonomy

- massive telemetry flows

That begins changing how infrastructure itself is designed.

The future AI stack may become increasingly distributed across:

- orbit

- edge devices

- robotics

- vehicles

- manufacturing systems

- autonomous operational platforms

Traditional cloud providers remain critical, but their role increasingly evolves towards:

- concentrated model training

- enterprise governance

- identity and policy enforcement

- historical analytics

- transactional resilience

Inference and operational intelligence may gradually decentralise outward.

Traditional cloud providers still dominate enterprise infrastructure today. Yet the combination of orbital compute, embedded AI chips, satellite networking, and persistent agents may gradually decentralise compute away from giant terrestrial regions.

The role of traditional cloud also starts evolving rather than disappearing entirely.

What traditional cloud infrastructure increasingly becomes

Traditional cloud increasingly focuses on:

- Massive model training clusters with concentrated GPU density

- Enterprise integration across ERP, EHR, CRM, and operational platforms

- Identity, RBAC, security enforcement, and enterprise policy management

- Long term analytics, observability, and historical storage

- Batch processing and asynchronous enterprise workloads

- API management, transactional systems, and operational resilience

Ironically, after years spent centralising infrastructure into giant cloud campuses, AI may decentralise computing again across orbit, edge, and distributed intelligence layers.

Infrastructure shifts often look obvious in hindsight. Slightly less obvious while people are still arguing about rockets on television.

Strategic Risks and Constraints

Of course, none of this is guaranteed.

Building a vertically integrated AI infrastructure stack introduces enormous complexity and risk, including:

- extreme capital intensity

- regulatory exposure

- infrastructure concentration risk

- geopolitical dependency concerns

- orbital governance challenges

- AI safety and autonomy questions

- semiconductor execution risk

The opportunity may be enormous. So are the implications.

Convergence, but not as we know it

Amazon is pursuing a remarkably similar trajectory through Project Leo, custom AI silicon, AWS infrastructure, robotics, and autonomous logistics. Blue Origin is also investing heavily in launch infrastructure and long duration orbital capability, while broader hyperscalers continue expanding edge AI, satellite partnerships, and distributed compute models.

That convergence matters.

When several of the world’s largest technology and infrastructure companies simultaneously begin aligning around low latency satellite networking, embedded AI chips, autonomous agents, robotics, and distributed compute, it usually indicates more than experimentation. It suggests the shape of the next infrastructure era is beginning to emerge.

The future AI platform may not be a single cloud region anymore.

It may become a globally distributed intelligence fabric spanning orbit, Earth, vehicles, robotics, and billions of autonomous systems operating continuously together.

References

- Reuters reporting on SpaceX, xAI, and Austin fabrication initiatives.

- Public xAI and Grok documentation covering agentic workflows, tool use, and multi agent orchestration.

- Public reporting on Starlink latency and Low Earth Orbit networking architectures.

- Tesla and Yahoo Finance reporting regarding A15 AI chip initiatives and embedded AI acceleration.

- Research notes and public reporting on Project Kuiper, AWS infrastructure expansion, and Blue Origin orbital initiatives.